Benefits of Triple Net Lease Investments

Investing in triple net lease (NNN) properties isn’t just about stable cash flow and minimal hands-on management. For many investors, the real incentive lies in the tax advantages that such structures offer. In this article, we’ll explore how NNN investments can be tax‑efficient, examine the IRS rules that govern them, and share strategies to maximize after‑tax returns.

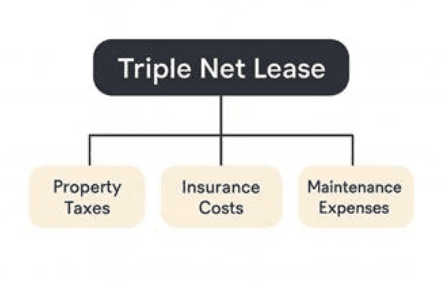

What Is a Triple Net Lease? Clarifying the Structure

A triple net lease (often referred to as “NNN”) is a lease structure in which the tenant agrees to assume responsibility for the three major variable costs of property ownership:

- Property taxes

- Insurance premiums

- Maintenance and repairs (including often structural and nonstructural)

Under such a lease, the landlord’s administrative burden is minimized: the landlord generally collects rent and ensures the tenant’s possession of the property.

Because the tenant bears most operating costs, the landlord’s income tends to be more predictable.

From a tax perspective, this “hands-off” structure is advantageous—but it also imposes some nuances.

Key Tax Benefits of Net Lease Properties

Here are the principal tax advantages that make NNN investments attractive:

Depreciation Shield

Even though a tenant pays operating expenses, the landlord retains ownership of the building and can claim depreciation. For nonresidential property, commercial real estate is typically depreciated over 39 years (straight-line) under IRS rules.

Because depreciation is a noncash deduction, it lowers the landlord’s reported taxable income without affecting actual cash flow. In many cases, taxable income (after depreciation and interest) ends up being much lower than the cash distributed by rent.

A cost segregation study can accelerate depreciation by reclassifying portions of the property (e.g. selective interior components, land improvements) into shorter lives (5, 7 or 15 years). These front‑loads deductions earlier in the holding period.

Interest Deduction

Most net‑lease acquisitions involve leverage. The interest paid on debt is generally deductible, further reducing taxable income.

Combining depreciation and interest, it’s possible that the property shows a paper loss (for tax purposes) even while producing positive cash returns.

Inclusion and Deduction of Tenant‑Paid Expenses

In triple net leases, tenants often reimburse or directly pay property taxes, insurance, and maintenance. Under IRS rules:

- Amounts paid by a tenant (or reimbursements) for expenses the landlord would normally have to pay must be included as rental income.

- The landlord may, in turn, deduct those same expenses (if ordinary and necessary) as rental expenses.

Thus, even though the tenant handles the operational costs, these flows are reflected in the landlord’s taxable income and deductions (assuming proper documentation).

Deferral of Capital Gains via 1031 Exchanges

One of the most potent tax tools for real estate investors is the § 1031 like‑kind exchange, which allows deferral of capital gains taxes if proceeds from a sale are reinvested in another qualifying property within strict timelines.

Because NNN properties tend to be stable, long‑term cash flow assets, many investors roll gains from one net lease into another, thereby continuously deferring the tax liability.

Treatment as Passive Income

NNN assets are usually passive investments (unless the investor qualifies as a real estate professional). Under passive activity rules:

- Losses (or deductions) can generally offset only passive income (not active income like wages), unless you qualify as a real estate professional.

- However, with depreciation and interest, you may reduce—or eliminate—taxable income even in a positive cash flow scenario.

In some circumstances, you might also benefit from the qualified business income (QBI) deduction (Section 199A), if your entity structure and income thresholds permit.

How IRS Rules Apply: Income, Deductions & Recordkeeping

Understanding how IRS rules apply to NNN properties is essential to sustain defensible tax positions.

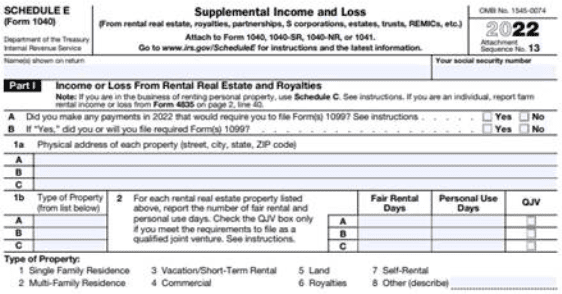

Reporting Income & Timing

- Rental income (including rent plus expense reimbursements) is typically reported on Schedule E (Form 1040) when the property is held as a passive rental.

- As a cash‑basis taxpayer (the norm), you include income when received and deduct expenses when paid.

- Advance rent must generally be included in the year received, regardless of the rental period it covers.

- Similarly, if you receive a payment for lease cancellation, that too is rental income.

Deductible Expenses

The IRS allows “ordinary and necessary” rental expenses, including:

- Mortgage interest

- Property taxes

- Insurance

- Repairs and maintenance

- Utilities (if landlord pays)

- Legal, accounting, and management fees

- Depreciation

- Travel related to managing the property

(Keep in mind that improvements must be capitalized, not deducted outright.)

If a tenant pays an expense that the landlord would otherwise bear, that amount is includable in income, but deductible as well (if valid) provided it’s properly documented.

Depreciation Recapture & Exit Implications

While depreciation provides a tax shield during ownership, on sale the IRS may apply depreciation recapture, taxing part of the gain as ordinary income (up to the amount of depreciation taken).

Thus, your exit strategy matters. Rolling into a new property with a 1031 exchange is often a key tool to avoid immediate taxation.

Recordkeeping & Compliance

Strong documentation is vital:

- Lease agreements, tenant payment records

- Invoices, receipts for maintenance, insurance, property taxes

- Depreciation schedules

- Accounting of reimbursements and expense flows

The IRS generally expects retention of tax documents for at least three years, though documents supporting basis or depreciation often should be kept longer.

Practical Considerations & Risks

Even with significant tax advantages, NNN investments carry risks and caveats:

- Because much of the operating cost burden shifts to the tenant, your potential deductions are more limited than in active real estate.

- If your tenant defaults or leaves, you may end up incurring costs you thought were off your plate (e.g. deferred capital repairs).

- Over-aggressive depreciation acceleration may backfire under audit or recapture.

- If the lease doesn’t clearly define which costs the tenant must pay, the IRS may challenge the net lease classification.

- Your ability to use deductions depends on your broader taxable income, passive income bucket, entity structure, and whether you qualify as a real estate professional.

Strategic Tips to Maximize After‑Tax Returns

- Commission a cost segregation study early to front‑load deductions.

- Framework your leases carefully to ensure clear, enforceable tenant‑paid expense clauses.

- Plan your hold period and exit structure with 1031 exchanges in mind.

- Monitor your tax status (passive vs active) and understand whether you qualify as a real estate professional.

- Maintain rigorous and well‑organized records to support deductions in the event of audit.

Why Net Lease Investments Are Tax‑Savvy

Triple net lease investments offer a compelling blend of passive income, low management burden, and tax efficiency. Through depreciation, interest deductions, reimbursement flows, and potential use of 1031 exchanges, investors can enhance net returns after taxes. That said, these benefits must be paired with careful tax planning, clear lease drafting, and prudent exit strategies.

You should always consult your tax professional regarding your personal tax situation, to ensure compliance with current laws and regulations as individual circumstances can vary.